Bjørn Lomborg is founder and president of the Copenhagen Consensus Center USA (CCC)), a tax-exempt 501(c)(3) “public charity” whose US physical presence is shown in the image: 262 Middlesex St, Lowell MA. Lomborg and the Copenhagen Consensus Center are known to DeSmog readers for efforts to downplay the importance of addressing climate change, a subset of climate science denialism that has infected the public debate across the English-speaking world.

Despite the name, it has not been based in Copenhagen since 2011. Deputy Director Roland Mathiasson remains there, but Lomborg moved to Prague in 2012. Workers seem mostly in Hungary, with a few in the US. The Board is Lomborg, Mathiasson, Scott Calahan (Ft Lauderdale) and Loretta Michaels (Washington, DC). Although some money is used for fundraising and PR in the US, much goes abroad to Mathiasson and Lomborg, who is said to travel 200 days a year.

The “real location” of CCC is unclear, and the Internal Revenue Service often cares about this with charities.

Copenhagen Consensus Center is a textbook example of what the IRS calls a “foreign conduit” and it frowns strongly on such things. It may also frown on governance and money flows like this, perhaps “inurement”:

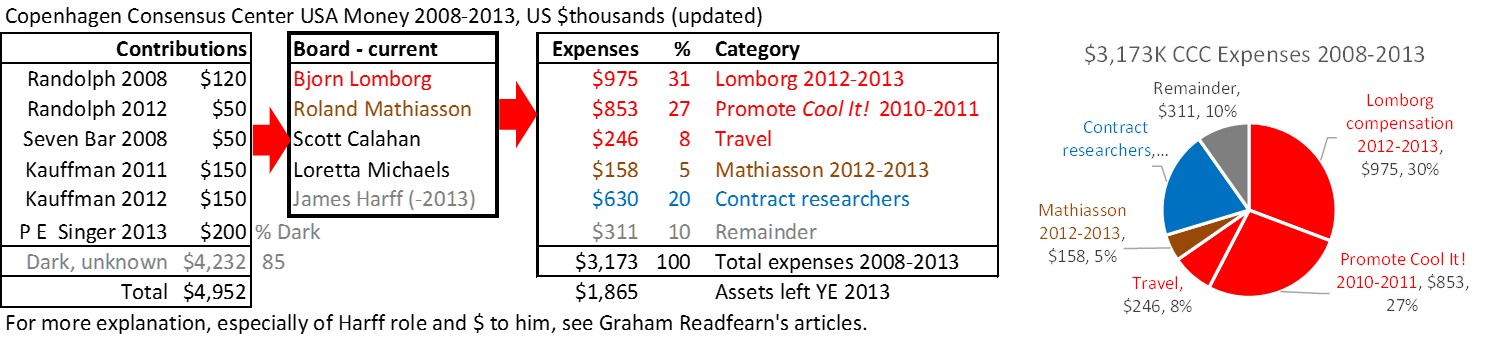

From attached Form 990 summary, more than 60% went directly to Lomborg, travel and $853K promotion of his movie. According to Wikipedia it grossed $63K and the movie poster shows a picture of Lomborg, a light bulb and heading:

“A LIGHT BULB WON‘T SOLVE GLOBAL WARMING

THIS GUY‘S BRIGHT IDEAS MIGHT“

Even in a simple US charity, poor governance and obvious conflicts of interest are troublesome, but the foreign element invokes stringent extra rules. Legitimate US charities can send money to foreign charities, but from personal experience, even clearly reasonable cases like foreign universities require careful handling. It is unclear that Lomborg himself is a legitimate charity anywhere, but most of the money seems under his control. One might also wonder where income taxes are paid.

A foreign group’s creation of a US “shell” charity to gather US funds and funnel them abroad is the most obvious of “foreign conduits” in IRS parlance, #1 on its list of no-no’s. IRS revocation of 501(c)(3) status not only eliminates tax breaks for ordinary donors, but eliminates entirely crucial major gifts from private foundations like the Randolph Foundation, Ewing Marion Kauffman Foundation and the Paul E. Singer Foundation.

CCC seems to break many rules. Foreign citizen Lomborg is simultaneously CCC founder, president, and highest-paid employee. Most people are a little more subtle when trying to create conduits, as in this example, where the IRS determined someone was not eligible for 501(c)(3) status, despite various stratagems to obscure the relationships.

Perhaps with his new $4 million Australia Consensus Center (covered here, here, here) Bjorn Lomborg may pick a better site than a US shipping storefront, since he’ll receive much more taxpayer money, directly, courtesy of the Australian government. That does seem simpler.

BUT UPDATE 05/08/15: University of Western Australia backed out after vociferous objections by faculty, students and many others. A derisive 05/05/15 Sydney Morning Herald article “View from the Street: So, is Copenhagen Consensus Centre just a US postbox?“ added many sarcastic Tweets to the furor. Unlike most this actually stirred Lomborg to a formal response ~05/07/15, annotated below, since it vaguely references this post.*** By the next day, it was over.

UPDATE 01/15/20: From CCC Form 2015-2017 Form 990s, we find Total Income, Lomborg’s Compensation and Travel

Income Lomborg Travel ($1,000s)

$2,940 $500 $195

$ 951 $600 $144

$2,559 $570 $184

Background details

Even before Lomborg’s recent Australia news, Graham Readfearn has done several fine investigations worth studying:

(1) The Millions Behind Bjorn Lomborg’s Copenhagen Consensus Center US Think Tank.

(2) Exclusive: Bjorn Lomborg Think Tank Funder Revealed As Billionaire Republican ‘Vulture Capitalist’ Paul Singer

CCC‘s EIN is 261214521 and one good source for its required IRS Form 990s is this, 2008-2013.

IRS issues for “public charity” think tanks were summarized in Fake science, fakexperts, funny finances, free of tax 2, pp.8-10, most of which dealt with more general issues, but at least two apply to CCC:

IRS-6G Governance needs to be active, engaged, independent The evidence offers reason for doubt.

IRS-10F Possible Foreign financial grant issues, not exempt Affects US organizations, but CCC even more.

Conduits – Google foreign charities IRS conduits

Following are a few of the many hits. This issue is widely understood, not obscure.

The IRS‘ Foreign Activities of Domestic Charities and Foreign Charities (pp.9-10) offers a succinct discussion:

“Rev. Rul. 63-252, in applying this principle to transfers of United States- solicited contributions from domestic to foreign organizations, concludes: …

‘Moreover, it seems clear that the requirements of section 170(c)(2)(A) of the Code would be nullified if contributions inevitably committed to a foreign organization were held to be deductible solely because, in the course of transmittal to a foreign organization, they came to rest momentarily in a qualifying domestic organization. In such case the domestic organization is only nominally the donee; the real donee is the ultimate foreign recipient.’

Rev. Rul. 63-252 then sets forth five examples of this point, each expressing a variation on the theme:

(1) A mere conduit entity formed by the beneficiary foreign organization in order to tap into United States resources; “

Gifts and Grants to Foreign Organizations, by Douglas A. Pressefall or Whyte Hirschboeck Dudek S.C. is a readable shorter article on the topic, including:

“However, there are unique issues that arise in the context of international charitable giving and grant making for the donor and the organizations the donors choose to support.

Charitable contributions that are made directly to a foreign organization by a U.S.. individual are generally not deductible for U.S.. federal income tax purposes. The same rule of non-deductibility applies to charitable contributions that are earmarked (or solicited by a U.S. organization) specifically for the use of a foreign organization.

However, a U.S. organization may solicit charitable contributions for its own exempt purposes and, in turn, choose to make gifts or grants to foreign organizations (e.g., Haitian relief). The U.S. tax treatment of those gifts and grants will generally turn on whether the U.S. organization has discretion and control over the contributions it received—in other words, in receiving or soliciting the funds, the U.S. organization cannot be legally bound to use the funds abroad if the donor is to be entitled to a charitable deduction; whether the foreign organization has a determination letter from the Internal Revenue Service (recognizing the organization’s tax exempt status); how the foreign organization intends to use the grant; and/or whether the U.S. organization is a public charity or a private foundation.

In Revenue Ruling 63-252, the IRS described five scenarios and the resulting tax consequences:

“Charitable Activities in a Foreign Country” Greg McRay, Foundation Group

“Grants by Public Charities to Foreign Organizations” The New York Community Trust

“international Giving By Public Charities” Guidestar

“International Philanthropy” The Law Office of Lisa Norton PLLC

CCC seems an obvious conduit organization, set up and led by a foreign resident to transfer money abroad, with poor governance and control.

For each person involved in CCC, either:

1) They knew perfectly well that the IRS routinely disallows this sort of thing when it notices, but the IRS does not have the resources to audit every 501(c)(3) that looks reasonable on paper.

2) Or were just completely uninformed about IRS rules, which may well apply to some of the young workers / volunteers.

CCC exists to tell the world how to spend money, but seems not to follow US rules for doing so itself.

Miscellaneous details from CCC‘s website and commentary

The home page features rotating pictures of poor children and their families. The donation page has similar images. While it does not say that money will actually go to helping such people, it is possible that members of the public might be misled into thinking CCC actually spends much money out there helping such people the way many real charities do.

For context about Lomborg’s efforts, people might read Lomborg and Playing the Long Game, inspired by Lomborg’s Book Cool It!

Despite owning both long UK edition and short US version, I had missed this in the Acknowledgments:

“I do want to say thank you…

to Richard Tol for making many of the economic arguments work better;

to Roger Pielke for many great suggestions for this book throughout the time I’ve known him;”…

One might wonder about the use of the term “consensus” for Lomborg’s work, , concurrent with efforts to attack or downplay the real scientific consensus on climate change.

The Contact page has an interesting history. At least until 11/29/14, one would not know it was in a storefront, unless one happened to use Google Street View to look for it:

“Please note, all physical correspondence will be electronically scanned and paper copies shredded. To ensure swift response, please only contact us by email or phone. We only accept unsolicited materials and queries via email.

Copenhagen Consensus Center

262 Middlesex St PMB SE-132

Lowell, MA 01852”

By 02/06/15, it explained that it used mail forwarding service, perhaps because the storefront got publicized. It said:

“By organizing ourselves as a network, we can work with the smartest people regardless of where in the world the might be located. Most of our core team, consisting of about 8 full-time project managers and communication people are working from Budapest. Despite the name we no longer have an office in Copenhagen. Our president and founder Bjorn Lomborg resides in Prague, but travels more than 200 days per year for conferences, seminars, meetings and interviews.”

In any case, according to IRS Form 990s, by 2015 CCC had moved to a different Neighborhood Parcel store:

1215 Main St PMB SE132

Tewksbury, MA 01876

The Board and Directors page gives, with annotations in Italics:

“Board & Directors

Bjorn Lomborg, President and Founder Prague

Roland Mathiasson, Executive Vice President, Secretary, and Assistant Treasurer Copenhagen, PR professional

Scott Calahan, Treasurer, Member of Compensation Committee, and Independent Director, Fort Lauderdale, FL

Loretta Michaels, Member of Compensation Committee and Independent Director, Washington, DC area*

Phone Number

Executive Assistant, Zsuzsa Horvath +1 347 903 0979 LinkedIn. ** Seems back and forth between NY and Hungary.

Advisory Panel

Professor Henrik Lando, Copenhagen Business School

Spence T. Olin, Professor Typo. North is Spencer T. Olin Professor, and Emeritus (born 1920).

Douglass C. North, Washington University in St. Louis

Professor Martin Paldam, COMMA“ Paldam is at the University of Aarhus, DK

*According to LinkedIn, Michaels is in Washington DC Metro Area, “working as a subject matter expert at the US Treasury.”

** This also shows links to others at CCC:

Elsebeth Soendergaard, Project Officer, Copenhagen

Steffen Wegner Mortensen, Junior Consultant at Rud Pedersen Public Affairs

Justin De Los Santos, Digital & Social Media Manager at Copenhagen Consensus Center, Hungary

Brad Wong, Strategy Consultant & Project Manager, Hungary

Ryan Betters, COO and Director of Partnerships (January 2015- onward), New York, interesting history

Examination of the 2012-2013 IRS Form 990s often showed only 2 employees (Lomborg and Mathiasson) plus 4-5 volunteers.

*** Following is annotated copy of Lomborg’s response, with my comments in Bold gray.

“Bjorn Lomberg’s response to Andrew P Street’s column

Andrew P. Street (“View from the Street”, May 4, 2015) criticises the Copenhagen Consensus Center, and in doing so makes many errors. Lomborg is entitled to his opinions, but read further to assess his claims.

He describes the planned research centre at University of Western Australia as a “climate change think tank”. As has been reported in this newspaper, Australia Consensus is not focused on climate change policy, but on broader development and economic policy. As discussed in Lomborg and Playing the Long Game, he employs subtle false multichotomies to avoid actions disliked by developed-world industries, conservative think tanks and politicians. What fossil energy group, especially coal, would ever object to Lomborg’s priorities?

This tactic somewhat resembles ways legislators add amendments to disliked bills to make sure they fail.He wrongly labels my 2010 documentary ‘Cool It’ as “anti-climate change”. The documentary actually explores responses to climate change, and the starting point is that global warming is real and poses a challenge to humanity. People might read either US or longer UK edition of Cool It! , watch the film, but also read this review at Yale Climate Connections. Saying global warming poses a challenge to humanity, but then doing everything possible to avoid effective policies is akin to saying that smoking is bad for health, but effective tobacco control measures like higher taxes are low priority. CCC did that, too.

Street misattributes to me the belief that “carbon pricing and emissions trading are more expensive than they’re worth”. I have long argued that well-designed carbon taxes achieve more good than they would cost. In UK Cool It!, check Index for “Carbon tax.” Lomborg focuses on a $2/ton CO2 tax, far lower than serious economists.

He states that the Danish state defunded the Center in 2011; this occurred in 2012. The Copenhagen Post Online 09/27/11 wrote Climate sceptic Lomborg may lose funding – New government plans to remove special funding to conservative commentators to save 100 million kroner” and DeSmog ran New Danish Government Axes Bjorn Lomborg’s $1.6 Million In Funding the next day. Perhaps money was left over, but this is at best an irrelevant nitpick, since the defunding handwriting was on the wall, and then Lomborg gave himself $775K in compensation in 2012.

The columnist makes the peculiar claim that “most of the work of the Center appears to take place in Hungary”. Copenhagen Consensus is a US-based non-profit organization with an international focus. Its work has been published by UK-based Cambridge University Press, and research conducted by more than 100 academics and 7 Nobel laureates. None live in Hungary. CCC‘s own webpage was quoted above: “Most of our core team, consisting of about 8 full-time project managers and communication people are working from Budapest.”

Most sinister is Street’s allegation – apparently copied from a climate change activists’ blog – that the Center is a “foreign conduit” designed to avoid taxation. This malicious claim is unsupported by facts. Copenhagen Consensus follows all rules governing its public charity classification and its tax-exempt status, neither of which have ever been questioned by relevant authorities. Did Lomborg actually read Street’s article, which linked to this post, the one that introduced the “foreign conduit” term to the discussion? If so, he knew the exact source and could have referenced it, which of course might have caused readers to visit this page. Instead, he dismissed it as “sinister” allegation “apparently copied” some unnamed “climate change activist.” I like California climate and am sad that it is changing, whereas Lomborg seems quite active in trying to make sure it does.

Of course, if Lomborg had a problem with my post, he might have contacted me or DeSmog.The IRS cannot audit each of the horde of 501(c)(3)s, so must rely on complaints by responsible citizens to highlight worthwhile cases. Even then, resources are limited, and as my father explained to me when he worked for the IRS, they must prioritize, sometimes on the basis of potential funds recovery. Smaller or soon-to-be-defunct groups may not be worth the bother In any case, readers are invited to follow the references here, assess the “foreign conduit” evidence and also read about “inurement” and $975K.

Street did not approach me or the Copenhagen Consensus Center before writing his column. We would have been very happy to correct his errors, and to tell him that we are, indeed, looking forward to an excellent partnership with civil society, researchers, and those on both sides of the political aisle in Australia.

What errors? Lomborg wrote this the day before UWA withdrew. Of course, the Australian government remains hopeful to find him a place better than the postbox/storefront in Lowell, Massachusetts.

Bjorn Lomborg, President, Copenhagen Consensus Center”

UPDATE 04/28/15: Add Cool It information.

UPDATE 05/01/15: Correct omissions of some other donors listed in Graham Readfearn’s articles.

UPDATE: 05/06/15: Add pie chart and colors to chart

UPDATE: 05/08/15: Add cancellation of ACC at University of Western Australia

UPDATE: 05/12/15: better image

UPDATE: 06/19/15: odd broken link for chart

Image: Ted Conference/Flickr, Google Street View.